- posted: Feb. 28, 2019

First and foremost, I want you to understand that there is absolutely nothing EASY or SIMPLE about today's world of health insurance or the companies that supply them. They are meant to be confusing and frustrating in hopes that the patient gets irritated with the provider, does not start or continue necessary care or follow through with their scheduled appointments or procedures (surgical or otherwise), which ultimately will save the insurance company money.

January 1 of each and every year is the most confusing time for just about everyone regarding, health insurance, their benefits, what they have to pay, when they have to pay etc., etc., etc.. I have been asked on average 12 times per day to explain a patients benefits (their insurance) so, I am hopeful for years to come that this provides some insight.

There are many factors in place that cause serious confusion and frustration for the consumer/patient. The confusion and frustration does not stop with you, I promise. Many providers have elected to leave health insurance programs completely and utilize a cash pay method. This is a much better decision for your everyday healthcare needs for many but it is completely misunderstood, and we will save that for another article. I am going to attempt to provide you with as much information, stated as simply as possible. I will be the first to tell you that the infographics contained are very misleading and will cause some extra confusion. Do not worry about those. Take a deep breath, sit back and get the scoop!

So let's take a look at "Fred," and his journey to necessary medical care while he insists on using his health insurance Fred hurt his leg.  He calls his doctor's office to schedule an appointment. 98% of all health insurance plans run January to December. However, there are a few that do not and start in June and go to June. That's another story for another day.

He calls his doctor's office to schedule an appointment. 98% of all health insurance plans run January to December. However, there are a few that do not and start in June and go to June. That's another story for another day.

Due to HIPAA (Health Insurance Portability and Accountability Act of 1996), health care providers must verify in person that you are who you say you are, with proof of your identity, such as your drivers license, etc. Do not get frustrated with your doctor's office that they cannot pre-verify your coverage, etc. By law they cannot take your health insurance information over the phone, especially they have never met you before. Again, they must verify who you are simply in order, to take your information, and verity your insurance.

The front desk will provide you with information to fill-out while they confirm your benefits (this is a time-consuming process as the staff either have to speak with someone directly at your insurance (it is amazing how calling back and asking the same questions to different people will, typically yield different answers), or they have to verify your benefits through an online portal. Doctor's offices are always told at the end that this conversation that the information provided is not a guarantee of payment and ultimately payment will be determined by the plan limits and exclusions (all of which is hidden from the doctors; your doctors, are driving blind with minimal information).

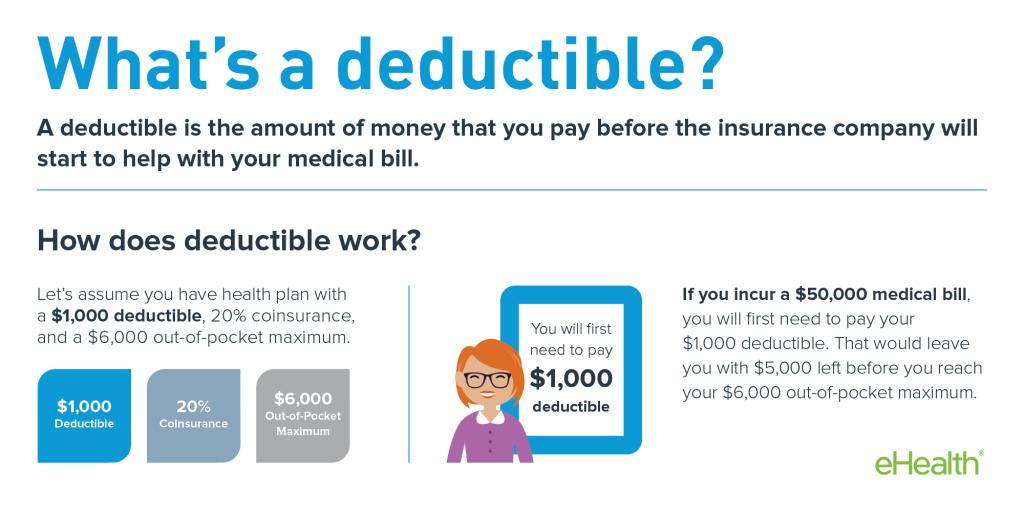

At this point, the doctor's staff will attempt to explain to you what they have found out regarding your benefits. If we are in January, you have likely not reached your deductible.

Thank you eHealth. The deductible, as it says above, is the amount of money that you will have to pay upfront before the insurance company will pay anything for your medical bills. This is important because if your bill today was $250 at the doctor's office, you will have to pay that amount in full, up-front. Some offices have different policies for what they will collect on that date of service, but expect to pay the minimum CASH visit fee for that day.

***EXCEPTIONS*** in rare cases, the deductible may not apply to specific provider or service types! This is where it gets difficult for the staff. Even though they ask the insurance company representative by phone, or review your benefits through the insurance company's online portal, they may not know the direct answer regarding your deductible until the Explanation of Benefits (EOB) arrives from your insurance company. Remember above: "This is not a guarantee……" blah blah blah. They really know how to make providers' and patients' lives difficult!

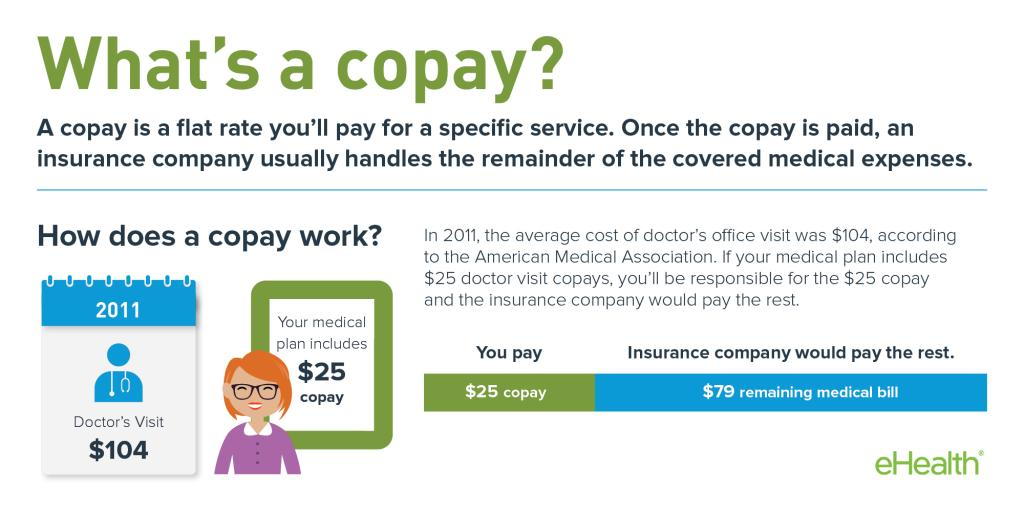

OK!!! We have moved through Step 1! What a headache that was.. So, assuming your deductible has been met, or it does not apply, then you may OR may not have a "co-pay". I know. I know. Wait, what's that???

Again, thank you eHealth. So the illustration above explains your co-pay, the "fixed" amount typically written on your card, that you will have to pay for today's visit….. Phew! That's over, now I can see the doctor right??? YES. At this point you can see the doctor and start the necessary treatment that you need..

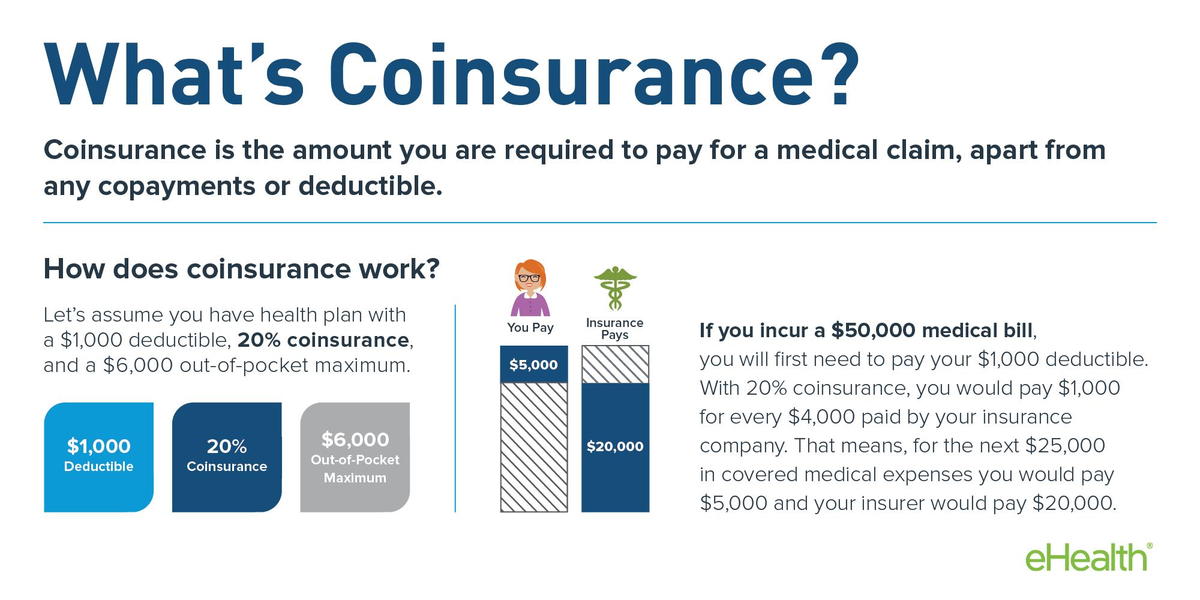

BUT WAIT!!! It's not over…. (It never is)… The insurance has this final issue called co-insurance that you must pay after your insurance has made their determinations of what they will pay and what YOU are ultimately liable for as part of your plan. So you may or may not have paid your "Deductible" for the visit, you have paid a "Co-pay" and now you get that "EOB" as discussed above, will have listed at the bottom "YOU MAY BE BILLED BY YOUR DOCTOR FOR THIS AMOUNT". This is your co-insurance.

Now don't get upset, this is your final payment for services.

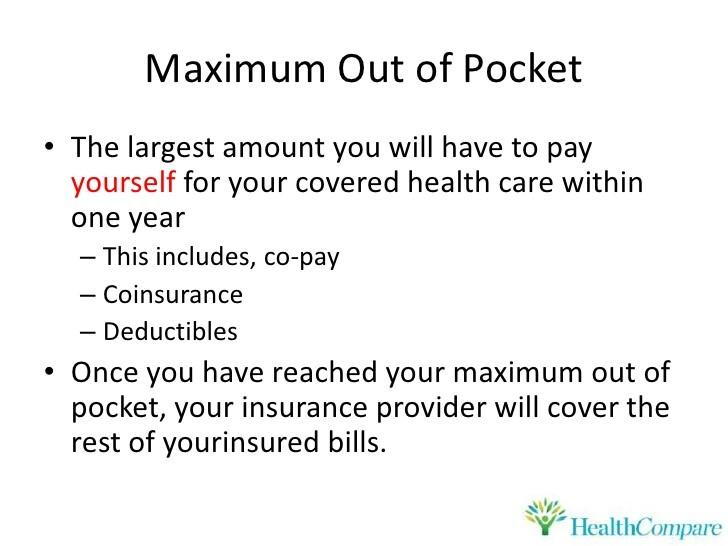

One last thing to understand is your "Out-of-Pocket Maximum". I know at this point you should be pulling your hair out, simply out of frustration. It's ok, I do it also, because every year EVERYTHING changes, it may not be drastic, it may be something tiny, but at the end of the day it affects your care and your limits. So what are Out-of-Pocket Maximums? ??

Thank you Health Compare! Once you have reached this amount (every plan varies) then you will no longer be required to pay during that annual term. (It's ok, just wait, January is just around the corner and its all about to start over).

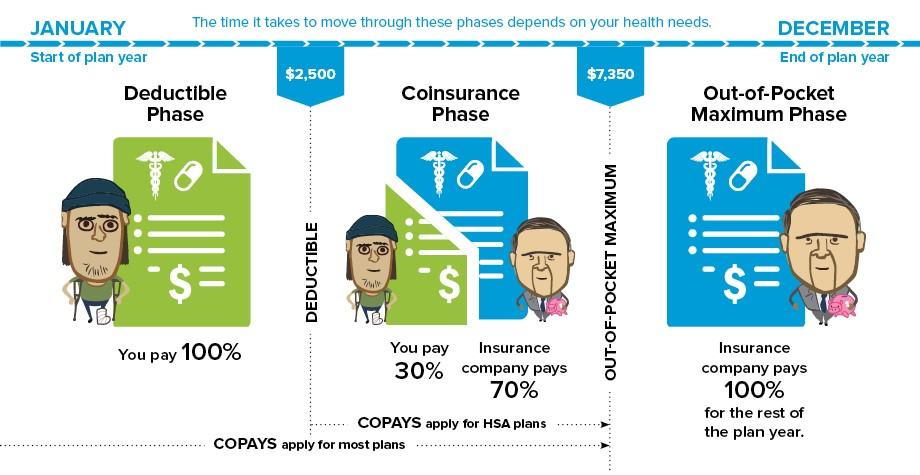

So, lets lay the entire picture out for you so that you can understand (at least attempt to understand) how your insurance works…..for the most part… as there are ALWAYS exceptions..

REMEMBER, THIS IS ONLY AN ILLUSTRATION. Your benefits may be different.

PLEASE, don't shoot the messenger, at the end of the day, this is YOUR insurance, YOU signed on the dotted line for it. Ultimately, I agree with you and your frustration! Your insurance agent or representative should have provided you ALL of this information and made sure you understood it before you left that meeting…but they handed you a book, and said to familiarize yourself with the rules, policies and other information contained there in. You likely, as did I, put it in a drawer and forgot about it.

Again, this starts over again in January for the mass majority of plans. The amounts and percentages will likely change annually as well.

Keep informed and don't get upset with the doctor's staff. They are simply doing their job and providing you with the limited amount of information that your insurance company gave to them, along with the "This is not a guarantee…." blah, blah, blah, disclaimer.

Please remember that when you receive a bill from the doctor's office, you have to pay that amount as part of your obligation to your insurance plan. Patients often complain, "BUT, doctor we pay so much for our insurance, you must charge too much" You don't want to see what an insurance company reimburses (or pays) the physicians for providing your care, surgeries and procedures. I hate to break your bubble but, it is so minimal that again, many doctors are opting out as providers. Honestly, most of you make more money per hour after the overhead is paid at a doctor's office.

So, go get the care YOU need. Be careful of the plans YOU choose. I hear everyday, "Well that was the free option." In most cases you, truly get what you pay for. At the end of the day, consider going into a cash payment plan with the doctor's office for things like regular treatment and/or inexpensive (less than $1000) procedures. It might save you money. Just remember that cash plans will not and cannot be used with, or sent to, your insurance to help with your deductible, etc..

If you would like to make an appointment for chiropractic treatment, give us a call 702-212-3333. We will be happy to work with you and provide you the most comprehensive information that allows you the care you need with the least amount of stress.

Location

Find us on the map

5650 W FLAMINGO ROAD

LAS VEGAS, NEVADA 89103, United States